Weekly highlights

- Asia-US West Coast costs (FBX01 Weekly) fell 4% to $4,905/FEU.

- Asia-US East Coast costs (FBX03 Weekly) climbed 13% to $6,095/FEU.

- Asia-N. Europe costs (FBX11 Weekly) had been degree at $4,491/FEU.

- Asia-Mediterranean costs (FBX13 Weekly) rose 6% to $5,135/FEU.

- China – N. America weekly costs decreased 4% to $6.62/kg.

- China – N. Europe weekly costs fell 10% to $3.63/kg.

- N. Europe – N. America weekly costs elevated 2% to $2.81/kg.

Dive deeper into freight information that issues

Keep within the know within the now with immediate freight information reporting

Evaluation

Some frontloading forward of a potential ILA port strike after January fifteenth and expectations of tariff will increase subsequent 12 months have saved transpacific ocean charges elevated to begin December, with charges to the West Coast – even earlier than the Lunar New Yr 2025 rush – already above their pre-LNY 2024 highs seen again in January at first of the Pink Sea disaster. Some carriers are reportedly introducing important GRIs to try to push charges increased to begin the month.

However the arrival window to maneuver shipments from Asia to the East Coast earlier than the strike deadline is closing, a major quantity of inventories had been already constructed up from frontloading forward of the October strike, and there’s probably nonetheless a runway of at the very least a number of months earlier than tariffs go into impact. These components might make early December charge will increase tough to maintain, although costs may enhance later within the month or early in January forward of Lunar New Yr.

Asia – Europe charges had been degree final week however have began to climb to this point this week, and each day costs to the Mediterranean are approaching the $6,000/FEU mark on December GRIs for a $1,000/FEU achieve in comparison with the tip of November.

If these will increase maintain, they could replicate a mix of efficient capability administration by carriers via a rise in blankings and an early begin to pre-Lunar New Yr demand. Guaranteeing mandatory orders are moved earlier than LNY is very necessary for shippers to the Mediterranean who’ve the longest further lead occasions attributable to continued Pink Sea diversions and, in the event that they miss that pre-holiday window, will face an extended wait for brand spanking new shipments to reach.

Carriers proceed to announce changes to their companies that may go into impact with the alliance reshuffle in February, with MSC including extra port pairs to its stand alone companies, and the Gemini Alliance already accepting bookings for its new hub and spoke mannequin.

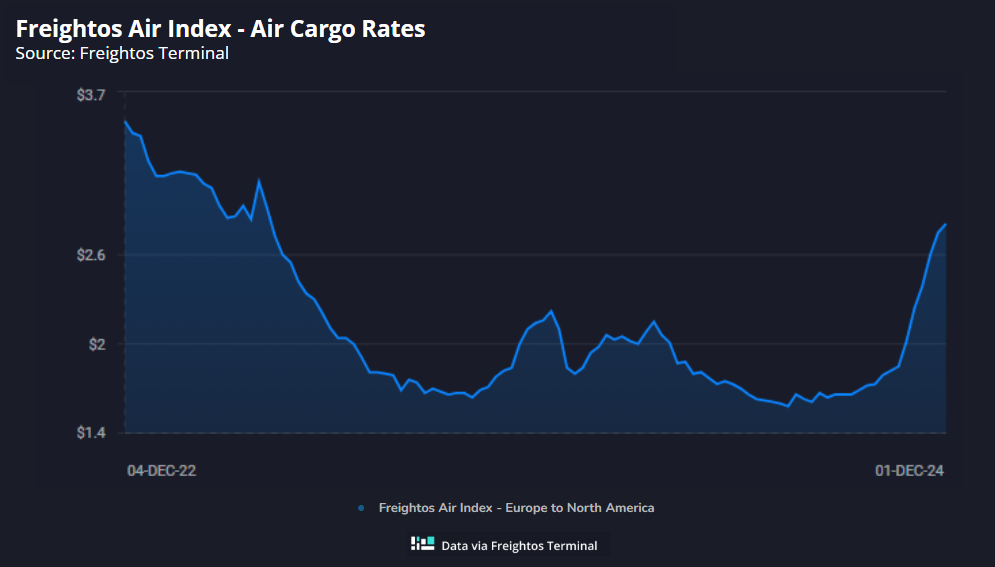

Freightos Air Index information present that ex-China charges to N. America and Europe have nonetheless not spiked, at the same time as we enter the important thing peak season weeks for early December. Along with some shippers’ and forwarders’ frontloading and securing capability prematurely, one other necessary cause for the comparatively tame peak season regardless of still-surging e-commerce volumes is carriers’ important shift of freighter capability to ex-Asia lanes in time for This autumn.

And with that capability being moved from lower-volume lanes, costs on these trades are rising. Transatlantic charges pushed previous $2.80/kg final week, 33% increased than a 12 months in the past and its highest degree since April 2023.

Freight information travels sooner than cargo

Get industry-leading insights in your inbox.