As actual property crowdfunding platforms go, Groundfloor is one in all my favorites.

It pays robust returns (an annualized common of 10%) with out the long-term dedication and requires simply $10 to start out. Diversification is straightforward, and the corporate has a powerful observe file of paying traders again.

Better of all, Groundfloor is open to everybody, not simply rich accredited traders. As for February 2025, it has accomplished over 5,800 initiatives with over $1.6 billion in retail quantity invested.

As you discover actual property crowdfunding choices, take a look at Groundfloor as a powerful contender.

Groundfloor Score

Abstract

Groundfloor pays robust returns with out the long-term dedication and requires simply $10 to start out. Diversification is straightforward, and the corporate has a powerful observe file of paying traders again. Better of all, Groundfloor is open to everybody, not simply rich accredited traders.

As you discover actual property crowdfunding choices, take a look at Groundfloor as a powerful contender.

Get Began with Groundfloor!

Professionals

- Brief Time period Investing

- Robust Returns

- Transparency in Returns and Efficiency

- Open to Non-Accredited Buyers

- Low Minimal Funding

- Automated Diversification

- Low LTV Loans

- Automated Investing Out there

- Weekly Repayments

Cons

- Lack of Liquidity (although primarily based on fractionalization, you will take pleasure in weekly repayments)

- Larger Threat in Cooling Markets

- Firm Not But Worthwhile

What Is Groundfloor?

![]()

![]() Groundfloor is a tough cash lender, writing short-term loans to actual property traders. Particularly, they supply purchase-rehab loans to each home flippers and BRRR traders. Additionally they present new development loans

Groundfloor is a tough cash lender, writing short-term loans to actual property traders. Particularly, they supply purchase-rehab loans to each home flippers and BRRR traders. Additionally they present new development loans

REtipster doesn’t present tax, funding, or monetary recommendation. At all times search the assistance of a licensed monetary skilled earlier than taking motion.

However they don’t have a vault of gold sitting round to fund all these loans. They increase a lot of the capital from folks such as you and me. By their award-winning actual property investing platform, they provide people the chance to pool funds and spend money on actual property initiatives with traders incomes repayments in properties relative to their funding quantity.

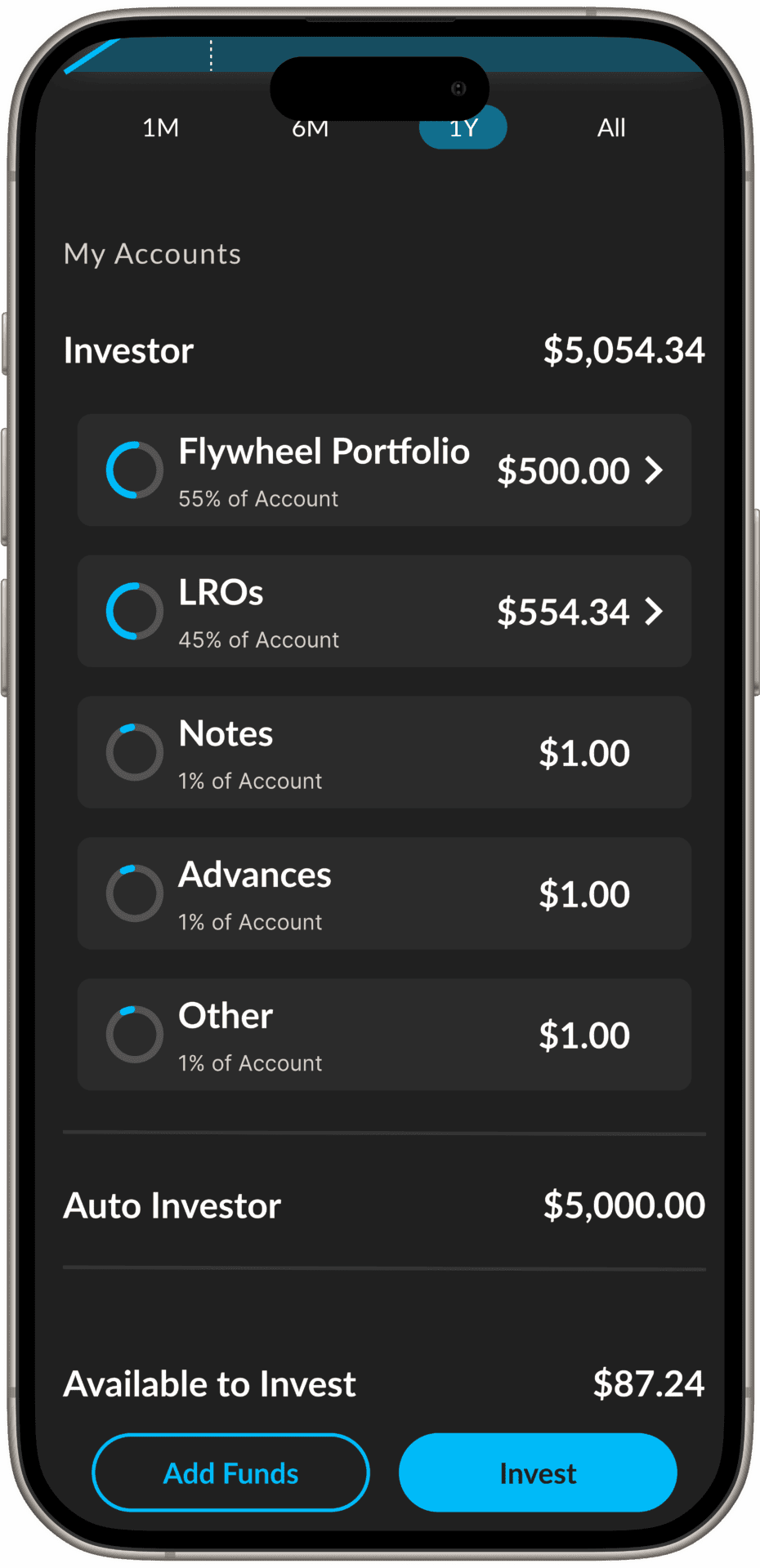

With the Flywheel Portfolio, you might be robotically diversified into 200-400 loans without delay, with fractions of a greenback going towards any single mortgage. This hyper-fractionalization and diversification helps to mitigate danger.

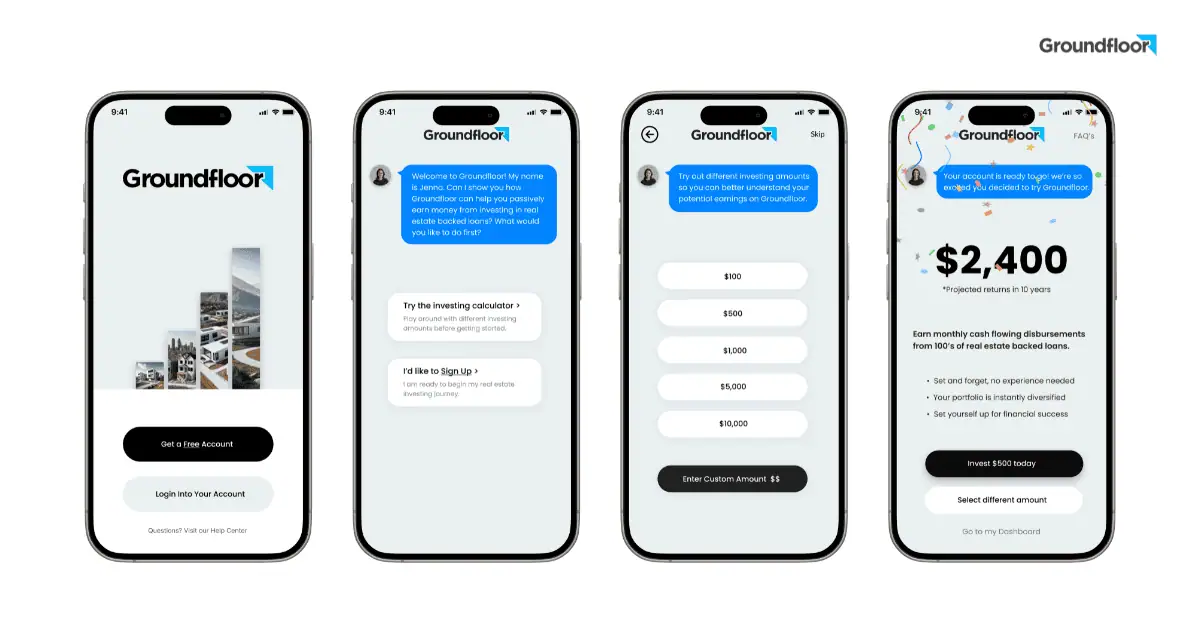

How Groundfloor Works

If you create an account with Groundfloor, you join your checking account to it so you’ll be able to simply switch funds forwards and backwards between the 2. When you switch cash to your Groundfloor account, you’ll be able to let Groundfloor deal with the work with their set-it-and-forget-it investing expertise, the Flywheel Portfolio, launched in October 2024. Right here’s the way it works:

- Groundfloor packages 200–400 short-term, high-yield loans into a group (the Flywheel Portfolio), providing instantaneous hyper fractionalization and diversification.

- Groundflooor originates and pre-funds these loans, and the Flywheel receives SEC qualification.

- Accredited and non-accredited traders alike can switch funds on a one-time or recurring foundation at a $100 minimal. These funds robotically make investments and get diversified throughout this portfolio of lots of of loans. Customers pay no charges upfront, however there’s a 0.50% to 1% administration price assessed on the time these funds are disbursed again to traders, together with their share of the curiosity. Groundfloor’s historic 10% annualized returns are included on this price.

- Buyers can see repayments in as little as seven days.

- Groundfloor boasts a powerful file with over 5,800 loans efficiently being repaid so far, indicating its dependability and stability instead funding avenue.

Groundfloor Professionals

Groundfloor is an funding platform with loads of benefits. There’s rather a lot to love.

Brief-Time period Investing

Groundfloor bucks the development that each actual property crowdfunding funding must be long-term. Regardless of my optimistic experiences with Fundrise, for instance, I don’t love leaving my cash invested for 5 years or getting hit with penalties.

All Groundfloor loans are short-term loans. You get your a refund in as little as seven days and luxuriate in constant weekly returns with the Flywheel.

Get Began with Groundfloor!

Assuming every thing goes to plan, after all. Not each investor pays again the mortgage on time, or in any respect for that matter. Sometimes, Groundfloor has to foreclose on defaulting debtors to recuperate their (your) cash.

The excellent news is that it’s nearly all the time in first-lien place on these loans, so their asset administration workforce is ready to yield robust outcomes from the underlying asset — the bodily property. That is why they’ve such a low loss ratio, as traders sometimes nonetheless recoup funds when properties go into default (though it could actually take longer).

Nonetheless, even within the worst-case situation, you aren’t a five-year dedication to become involved.

Robust Returns

In my expertise with Groundfloor, I’ve earned a median return of round 9.5% every year. That aligns with their common historic annualized all-time return of round 10%.

In my expertise with Groundfloor, I’ve earned a median return of round 9.5% every year. That aligns with their common historic annualized all-time return of round 10%.

From January by means of January 2025 (the newest knowledge obtainable at this writing), they’ve returned a median of 9.88%.

These numbers might not get your blood pumping like a canine in warmth, however they’re nothing to scoff at. They’re in keeping with common inventory market returns, besides with out the wild temper swings and volatility, plus you might have regular funds.

Transparency in Returns and Efficiency

Groundfloor wins prime marks for transparency.

You earn the mortgage rate of interest, interval. They don’t take any charges upfront to spend money on the Flywheel. As an alternative, the Flywheel administers a administration price of 0.50% to 1.0%, assessed on the time these funds are disbursed again to you, alongside together with your share of the curiosity.

Evaluate this price and return the construction to HappyNest, with its price data buried within the legalese of their SEC round.

I additionally like that Groundfloor publishes month-to-month efficiency studies on what number of loans they funded, what number of loans had been repaid, and the rates of interest of these loans. On the uncommon event that I’ve contacted Groundfloor to ask for extra details about their efficiency, they’ve rapidly responded and equipped it.

Open to Non-Accredited Buyers

Many actual property crowdfunding platforms solely enable accredited traders to take part. It makes for simpler regulation on their half, nevertheless it leaves most Individuals unable to speculate.

Groundfloor lets anybody make investments, with minimal money in addition.

Low Minimal Funding

Not many investments allow you to get began with $100.

Together with your $100 minimal funding, Groundfloor allows you to make investments into 200-400 loans without delay, eradicating any excuse that you just “can’t afford to speculate.” Skip the lattes this week and make investments some cash in actual property!

Simple Diversification

That low minimal funding in every mortgage makes it simple to unfold your cash amongst many alternative loans secured by properties nationwide. With the Flywheel Portfolio, you’re immediately invested and robotically reinvested into a group of lots of of loans.

I do know {that a} sure small proportion of those loans will default and gained’t pay me the total curiosity promised. That’s the place the Flywheel Portfolio shines. The moment diversification into a group of lots of of loans helps mitigate this danger. However most pays as promised, so the occasional low or unfavourable return will simply mix into my common returns every year.

Low LTV Loans

Groundfloor underwrites loans at a comparatively low proportion of the property worth as a tough cash lender.

If the borrower defaults, that leaves loads of fairness for Groundfloor to recuperate the mortgage in the event that they take a deed as a substitute of foreclosures or, within the worst-case situation, foreclose on the property.

Within the three years I’ve invested with Groundfloor, I’ve by no means misplaced cash on mortgage. The worst that’s occurred has been a return on my unique funding with no curiosity.

Automated Investing Out there

The Flywheel Portfolio, Groundfloor’s hottest product, presents automated investing and reinvesting for constant compounding, annualized 10% returns.

Get repaid weekly and may elect to have your returns reinvested into initiatives, right down to even fractions of a cent.

Groundfloor Cons

Each funding has its downsides, or else traders would flock to it, and abruptly it wouldn’t need to pay excessive returns anymore.

Hold the next drawbacks in thoughts as you think about investing in Groundfloor.

Lack of Liquidity

If you spend money on a mortgage on Groundfloor, you commit your cash till the mortgage repays. Each time which may occur, there’s no method to pull your cash out of a mortgage early, although you get weekly repayments with the Flywheel Portfolio.

Most loans repay on time, or at the least near it. However a big minority of debtors don’t promote or refinance their loans on time, and also you get your a refund later than anticipated.

Larger Threat in Cooling Markets

Low-LTV laborious cash loans don’t include many dangers when housing markets growth at 5% to twenty% appreciation.

However when residence costs cool off, abruptly these low-LTV loans don’t look fairly as bulletproof. As an alternative of your mortgage making up 70% to 90% of the property worth, it would make up 80% to 100% of the newly cooled worth, which doesn’t go away a lot (if any) leeway ought to it’s a must to foreclose to recuperate your cash.

Firm Not But Worthwhile

Regardless of elevating billions of {dollars} in laborious cash loans, Groundfloor has by no means turned a revenue. That ought to offer you pause as you think about investing cash by means of their platform.

Granted, a lien backs your funding towards a selected property. Even when Groundfloor goes bankrupt, you’ll nonetheless obtain your a refund when the borrower repays the mortgage. However a lender in chapter isn’t precisely the regular hand you’d wish to deal with loans that default.

In some unspecified time in the future, Groundfloor will both flip a revenue, or their traders will run out of endurance and cease funneling cash into them.

How Groundfloor Compares

Groundfloor presents excessive returns on short-term investments—a mixture you don’t see fairly often.

You’ll be able to doubtlessly earn larger returns by means of actual property fairness platforms like Fundrise, the place Seth earned a median return of 14% over 5 years. However it’s essential to go away your cash invested long-term, paying the penalty in case you withdraw in below 5 years.

I’ve collected robust dividends from Streitwise, averaging 8.4% over the previous few years. However they, too, include a long-term dedication and early withdrawal price and have underperformed Groundfloor’s 9.5% to 10% returns.

In case you want quick liquidity, attempt Concreit or Stairs. Neither pays as excessive returns, however you’ll be able to pull your cash anytime.

Ultimate Ideas

General, Groundfloor stacks up properly in transparency, returns, and lack of a long-term investing dedication.

Whilst you don’t instantly profit from actual property appreciation such as you would in an fairness funding, you’ll be able to accumulate robust curiosity backed by an actual property lien. I’ve discovered Groundfloor to supply moderate-to-high returns with low-to-moderate danger—a ratio I’ll take any day.

Get Began with Groundfloor!

The best danger with Groundfloor loans lies in a housing market collapse. If we had a 2008-style actual property disaster, with residence values falling by double digits and mass foreclosures, lots of your Groundfloor loans would lose cash. That stated, you’d nonetheless get one thing again in your mortgage investments after Groundfloor forecloses to recuperate as a lot of your funding as potential.

Regardless of housing markets cooling from their overheated pandemic highs, the U.S. nonetheless has a housing scarcity. I don’t see an actual property market collapse on the horizon, and I really feel assured that I’ll get my Groundfloor investments again with robust curiosity.