What I am eager about: Unprecedented (and shaky) macro circumstances and the elite decision-making and resilience wanted to win on this atmosphere.

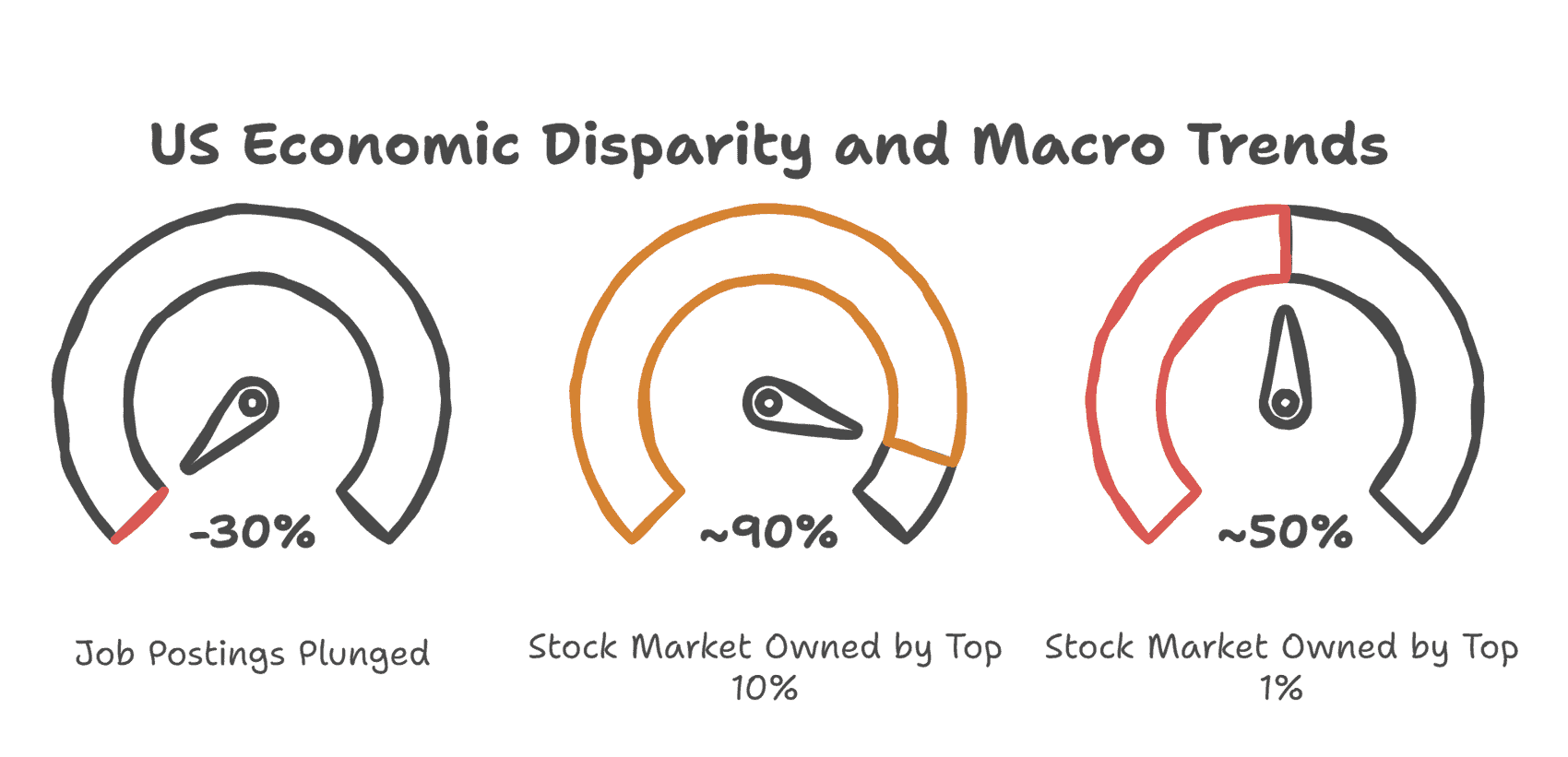

Job postings have plummeted 30%, in line with Certainly, from their peak over the last charge adjustment interval. ADP reported the U.S. misplaced 32,000 personal sector jobs in September. Hiring charges hit 2008-2009 ranges.

But the inventory market retains climbing, GDP development appears strong, and company earnings are at an all-time excessive. Most of that is pushed by AI, which is sort of inconceivable to scale back or remove funding publicity from, irrespective of which sector you deal with.

It’s price mentioning that about 90% of the inventory market is owned by the highest 10% of U.S. households, and round 50% by the highest 1% of U.S. households.

If you happen to hadn’t heard that earlier than, it makes you do a double-take, proper?

RELATED: 236: Callan Faulkner 5X’ed Her Income with AI. Right here’s How You Can Too

These numbers get thrown round typically, however I attempt to remind myself of this routinely, given the implications for the inhabitants at giant and general shopper spending. So I put extra weight on the macro components which might be impacting a a lot bigger portion of the inhabitants (~300 million folks).

Let’s begin there.

(BTW, for a easy studying expertise, I’m not overloading you with hyperlinks for the stats. Be at liberty to substantiate by yourself, after all.)

Early Indicators of Market Alternative

I’ve observed a transparent shift within the ~2x margin offers making it to the closing desk for acquisition. Monetary misery is ruling the roost once more (e.g., troublesome mortgages/liens/taxes, healthcare payments, household heirship conditions normally accompanied with cash bother, and so on.)

The “I had plans to construct, however I am not shifting again to the realm” sellers? They nonetheless exist, however they’re much less frequent, or they’ve that rationale but in addition have a finance concern.

Macro-wise, we’re seeing early indicators of elevated misery. FHA mortgage (first-time or lower-income house patrons) delinquencies are at 12%, as excessive as they had been throughout the GFC. Google search quantity for “assist with mortgage” is almost as excessive as throughout the GFC. One-third of U.S. adults skipped wanted healthcare resulting from price over the past 12 months. Cardboard field manufacturing is down 9% in 8 months (double the GFC decline). Pet shelter intakes are surging.

Financial cracks are widening. Extra sellers will want exits (and land is first to go in comparison with properties). Affected person capital wins.

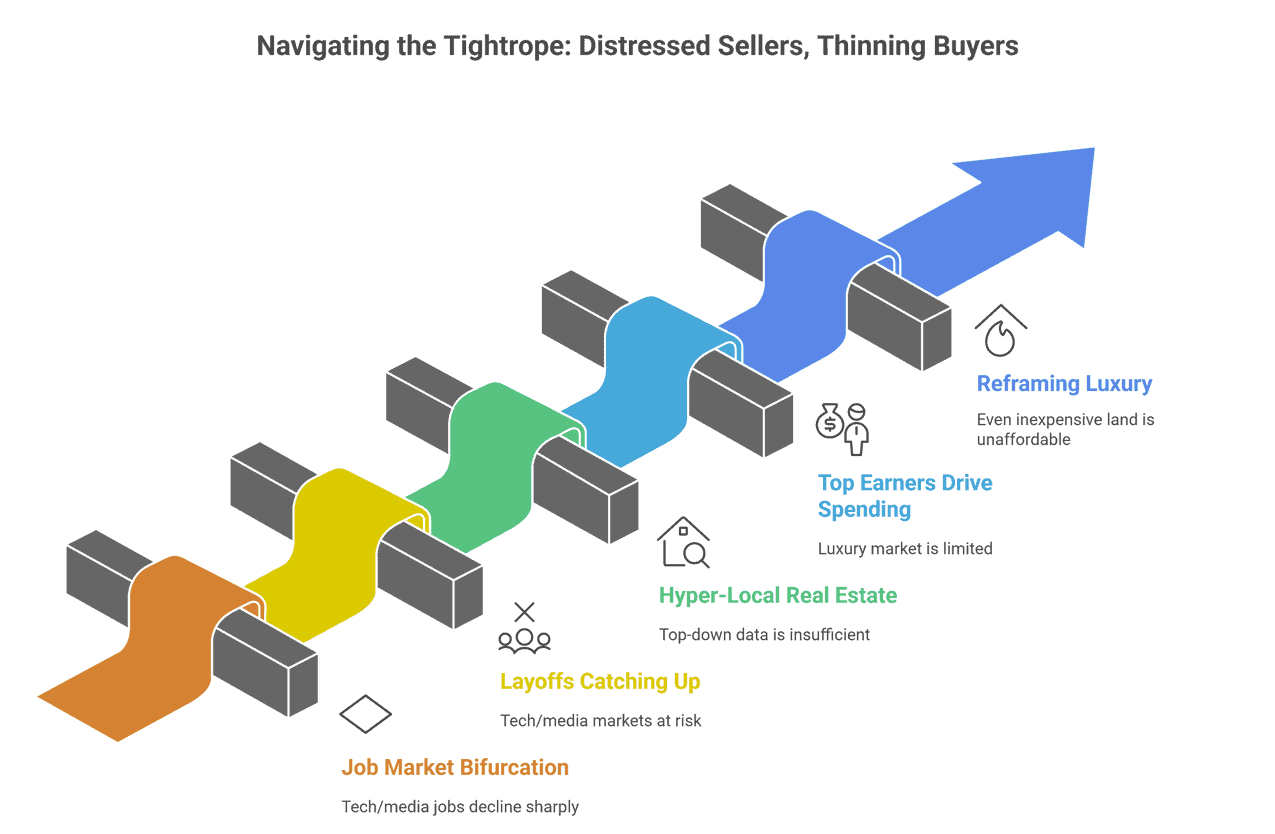

Understanding the Shrinking Prosperous Purchaser Pool

Whereas distressed sellers create alternative, the client pool is shrinking concurrently. That is the tightrope we’re strolling.

As an illustration, job market bifurcation is excessive. Healthcare job postings are up 38% from pre-pandemic, and job openings for therapists and physicians are up roughly 85% every (my spouse, who’s a medical therapist, cherished this information). Software program growth is down 37%; media and communications are down 36%; advertising is down 23%.

Whereas layoffs haven’t but caught up with the lower in hiring, investing in offers in closely tech and media-exposed markets like California will be dangerous. Conversely, markets close to main hospital techniques and healthcare hubs (e.g., Boston, Cleveland, and Houston) present extra resilience.

Critically, jobs information alone does not decide housing markets (as at all times, actual property is hyper-local, and bottom-up information at all times trumps top-down), you might want to pair employment developments with days-on-market, stock ranges, and pricing strain. For instance, Illinois is internet shedding jobs, however properties transfer in 38 days on common, with the bottom out there stock within the U.S.

One other key stat that ought to be imprinted in your thoughts: The highest 10% of US earners now drive 50% of all shopper spending. That is up from 36% three a long time in the past, per WSJ.

Take into consideration what meaning for land: We’re not promoting to the common American. We’re promoting a luxurious product to roughly ~30-35 million individuals who can really afford it. Everybody else is barely hanging on.

And ensure to reframe what “luxurious” really means. When the median U.S. family can solely cowl a ~$500 unplanned expense, even an “cheap” $5-10K land parcel is out of attain for many patrons outdoors of proprietor financing.

Why Aggressive Gross sales Groups Cannot Power Market Demand

I’ve seen some land operators just lately seeking to rent a VP of Gross sales or construct aggressive dispo groups. And I preserve questioning… how cost-effective is that basically?

We think about ourselves to be dispo consultants (with tens of millions in gross sales to again that up), and you may exhaust most dependable purchaser channels fairly shortly:

- MLS (~80-90%+ of actual property transactions)

- Land.com, FB, and comparable platforms

- Focused chilly name/textual content/mail to space residents and up to date acreage patrons

- Indicators and native advertising

- Builder/developer outreach

- Auctions (break in case of emergency)

We’ve tried all of these, with various outcomes. As soon as you have hit these channels, what’s left? Mailing each family within the township? Calling/texting each individual within the county? Door-to-door gross sales?

The price explodes when the online margin is already tight from an acquisition price perspective. The focusing on deteriorates. You are reaching for more and more unqualified patrons.

Because the above part notes, land is a luxurious good. Take into consideration Burberry or Louis Vuitton. They do not ship door-to-door salespeople. Their killer manufacturers do loads of the heavy lifting for them, however even they don’t have infinite margin to push gross sales.

In a patrons’ market with a constrained 10% prosperous purchaser pool, you’ll be able to’t drive gross sales by means of sheer gross sales horsepower. You want the appropriate product, the appropriate worth, the appropriate location, the appropriate purchaser channels, after which endurance.

Happily, land usually has low holding prices. So if you might want to wait out a market (and worth cuts aren’t efficient), then wait it out.

If I am lacking one thing right here, I am genuinely open to suggestions. However I’ve talked to among the finest operators within the area, and nobody’s cracked the code on cost-effective hyper-aggressive dispo on this atmosphere that may inevitably get any piece of stock to maneuver within the face of a tricky market.

Selective Underwriting and Market Adaptation

We proceed to strategy this market with excessive warning paired with opportunistic motion. Nonetheless funding offers, however solely the apparent 2X gross margin performs with bulletproof draw back safety.

We (proceed) to tighten up underwriting: Backside 25% of traits? Will not contact them, no matter worth.

We’re looking distressed sellers in markets the place the highest 10% purchaser pool stays secure. Following job development/loss information. Watching days-on-market like a hawk.

The alternatives exist. They’re simply more durable to seek out and require extra self-discipline to underwrite accurately. And we accomplish that nicely as a result of nobody on our group is “above” the work required to win. Everybody will get their palms soiled. There are not any shortcuts.

It is laborious to make macro-level financial predictions, however I count on an general tougher dispo marketplace for at the least the foreseeable future. I’d LOVE to be improper, clearly, and for a bull market to return again round sooner. As an apart, loads of of us are nonetheless greedy for the expectation that reducing rates of interest will allow one other actual property increase. I am much more cautious about that. It’ll actually be useful, however I believe the impact shall be minimal to modest at finest, particularly after we noticed important charge cuts over the last charge adjustment interval and actual property demand continued to say no.

Many operators will wrestle or crash out of the trade.

Those who modify — those that pair distressed vendor sourcing with maniacal purchaser pool evaluation and keep strict underwriting even when capital is burning a gap of their pocket — will feast.

=====

Searching for funding from a group that understands either side of this buyer-seller equation? Severe Land Capital is actively in search of offers with real 2X margins and draw back safety. We’re not sitting on the sidelines, however we’re additionally not pretending the macro does not matter.