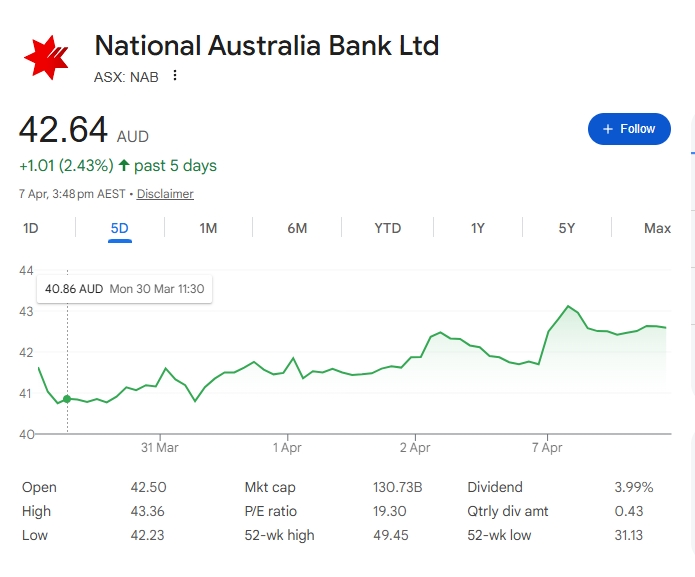

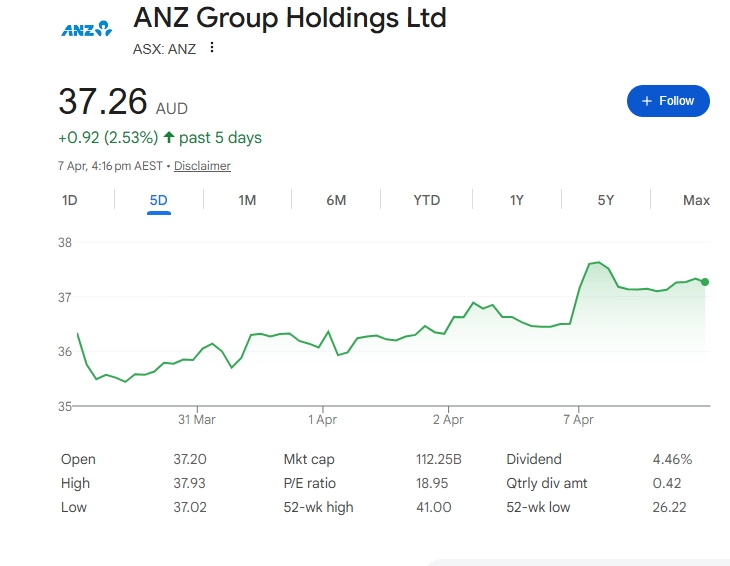

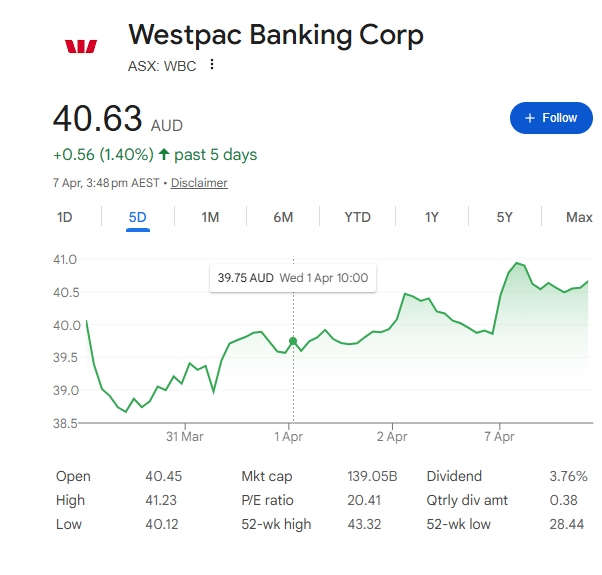

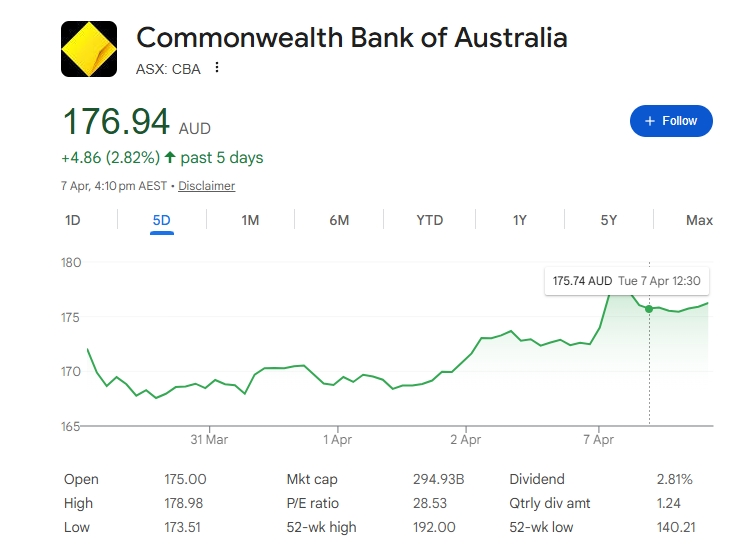

What I stated a couple of days in the past, trying on the RBA’s 2026 surcharge reform, was that “the large banks… are definitely winners,” regardless that many stated it regarded unfavourable for his or her payment earnings so disputed my declare. Listed below are some attention-grabbing charts of Financial institution Shares over the previous few days. The RBA choice was introduced on 31 March, and all the large banks’ share costs have been up since then. Examine them out right here, the RBA choice was on thirty first March. Can anybody title any main purpose for these value rises on this interval apart from the RBA choice?

Key takeaways

- The RBA’s March 2026 conclusions paper confirmed a ban on surcharges from 1 October 2026.

- The identical bundle additionally consists of decrease interchange charges and stronger transparency guidelines.

- The announcement regarded unfavourable for financial institution payment earnings on the floor.

- Main financial institution shares nonetheless rose after the RBA announcement.

- That market transfer suggests traders might have anticipated a worse consequence.

- Retailers nonetheless want to arrange for the lack of seen card surcharges at checkout.

- POS reporting and service provider payment evaluate will matter extra as soon as the ban begins.

What’s the 2026 RBA surcharge ban?

The 2026 RBA surcharge ban is a funds reform that ends card surcharges on debit and bank card transactions from 1 October 2026, whereas additionally decreasing some interchange payment caps and enhancing payment transparency. The RBA set out that route in its March 2026 conclusions paper after session.

First, this was not only a free dialogue. It was the RBA’s closing public place at that stage, and the market handled it as a concrete coverage choice. A retailer that when added a 1.5 p.c surcharge on the terminal might want to take away that cost and rethink the way it recovers fee prices.

Why did financial institution shares rise?

Financial institution shares rose as a result of the market possible noticed the ultimate bundle as much less damaging than feared. When traders hear a reform that might lower payment earnings, they don’t solely ask whether or not it’s unfavourable; additionally they ask whether or not it’s higher or worse than what that they had already priced in.

Subsequent, that issues quite a bit. If merchants anticipated a harsher crackdown on financial institution and funds income, then a extra restricted bundle can nonetheless push shares increased. In different phrases, a “unhealthy” coverage can nonetheless elevate shares if it was not as unhealthy because the market feared.

Why did the response look odd?

The response regarded odd as a result of the announcement clearly affected payment earnings, but the financial institution sector nonetheless went up after the information. The traders didn’t learn the reform as a catastrophe.

Furthermore, that is the place the story will get attention-grabbing. If the RBA’s bundle had actually threatened financial institution earnings in a serious approach, you’ll anticipate a a lot clearer unfavourable market response. As a substitute, the share value transfer implies traders both anticipated worse or believed the impact could be manageable.

What does the share transfer imply?

The share transfer might imply traders thought the banks may take up the change. It might additionally imply the reform leaves the broader card system intact, which protects transaction volumes even when some payment settings are trimmed.

For instance, a financial institution can lose some surcharge-related or interchange-related earnings and nonetheless look sturdy if card use stays excessive. That’s the reason the market can deal with the reform as a short-term unfavourable however a longer-term non-event, or perhaps a delicate optimistic.

Why this issues for retailers

Retailers mustn’t confuse a bank-share rally with a win for retailers. The truth that shares rose doesn’t imply the reform routinely helps small retailers.

As a substitute, the sensible challenge is that retailers lose a visual strategy to get better card prices. A store that used to indicate a card surcharge at checkout will want one other strategy to defend margin, whether or not via pricing, payment negotiation, or tighter price management.

What adjustments on the checkout

The most important change for retailers is the checkout expertise. The surcharge line disappears, however the underlying fee price doesn’t.

Which means retailers want to grasp the complete price of taking playing cards, not simply the seen payment handed to the client. A POS system that reveals payment-type gross sales, common transaction worth, and card-cost impression turns into far more helpful as soon as surcharging is not out there.

Find out how to put together

Retailers ought to evaluate their service provider statements, terminal charges, and POS reviews now. The aim is to know precisely what card acceptance prices earlier than the October 2026 deadline.

Tip: Put together early by analysing how a lot every fee technique prices your enterprise. This makes it simpler to plan different restoration methods when surcharges are gone.

Subsequent steps

Clearly, now we have questions in regards to the RBA’s rationale for its choice, however the speedy level for retailers is that the inventory market shouldn’t be your most important downside right here. Your actual challenge is the best way to handle fee prices when you may not add a visual surcharge at checkout. The RBA choice ought to cut back financial institution charges, assist alleviate a few of the payment variations confronted by small and huge retailers, and supply higher transparency into financial institution charges.

Retailers ought to take 4 steps earlier than 1 October 2026:

- Overview present service provider charges and terminal expenses.

- Examine POS reporting for payment-method visibility.

- Revisit pricing to ensure margins nonetheless maintain.

- Discuss to fee suppliers about lower-cost options or higher payment transparency.

Put together your store for the 2026 RBA surcharge ban

Replace:

Replace:

For the reason that article first went dwell, it has develop into a sizzling matter. A number of have questioned the hyperlink between the 2026 RBA surcharge ban and the rise in financial institution shares. That could be a truthful level, and it’s value explaining the information in plain phrases.

First, it’s true that Suncorp’s share value fell throughout this era, which at first look appears to contradict the concept the RBA choice helped banks. However Suncorp is not a standard financial institution for many traders. Suncorp Group bought Suncorp Financial institution to ANZ in 2024, took the cash, and later returned money to shareholders. In the present day, the listed firm is extra of an insurance coverage enterprise than a financial institution, so its share transfer doesn’t inform us a lot about traders noticed the surcharge ban.

Second, the great share response was not simply in banks. Fee corporations listed on the ASX, corresponding to Tyro and SMP, additionally rose after the announcement.

Third, that the banks’ shares rose due to the higher revenue numbers they introduced again in February and the curiosity‑price transfer in March. That’s true, they did rise, however right here the timing is an issue. We are actually in April, and people revenue updates and the March price transfer occurred earlier. If these have been the explanations, you’ll anticipate the share value elevate to indicate up in February and March, not now in April. As a substitute, the rise strains up most carefully with the announcement of the 2026 surcharge ban. Additionally you’ll want to clarify why traders reacted the identical strategy to non‑financial institution corporations in Debit and Credit score Crads. Funds gamers like Tyro and SMP noticed their shares rise too, regardless that they don’t profit from the identical upside from financial institution‑fashion earnings or price adjustments.

Third, traders favored that the surcharge ban applies to each debit and bank card transactions from 1 October 2026. When the additional checkout payment disappears for each, clients have the identical value whether or not they use debit or credit score. That may make individuals extra possible to make use of bank cards, as a result of the “additional price” they used to see is gone. That is what we acknowledged in our submission right here. Extra bank card use means increased charges. The traders would even have favored the financial institution’s feedback that new charges will should be created or some charges will should be elevated to cowl the loss.

All of this doesn’t weaken the article’s authentic level. It simply sharpens it. The traders see the ultimate bundle as optimistic and manageable relatively than an enormous hit.

Written by:

Bernard Zimmermann is the founding director of POS Options, a number one point-of-sale system firm with 45 years of trade expertise, now retired and in search of new alternatives. He consults with numerous organisations, from small companies to giant retailers and authorities establishments. Bernard is obsessed with serving to corporations optimise their operations via revolutionary POS know-how and enabling seamless buyer experiences via efficient software program options.