The restaurant business’s aggressive panorama for mealtime {dollars} is altering quick, and it is not model in opposition to model. More and more, grocery and comfort shops are stealing share by providing fast, reasonably priced, and more and more high-quality meal choices.

In Income Administration Options’ (RMS) latest shopper report, Verify, Please or Verify Out, 24 p.c of surveyed diners say they purchase meals from grocery shops extra regularly than a yr in the past. This represents a bigger improve than these rising visits to fast-casual (14 p.c) or full-service (11 p.c) eating places and is on par with these visiting QSRs extra regularly (24 p.c) (RMS Q1 2025 Eating report). The two,000 U.S. customers surveyed additionally hit up comfort shops for meals 15 p.c extra typically than previously.

The findings reinforce a key reality: worth and comfort drive selections and restaurant operators should reply or danger dropping floor.

The Rise of the Retail Meal

When requested about their major motivation for rising their purchases, respondents reported worth for the cash and ease.

Grocery and c-store rivals acknowledged the chance. Pre-packaged meals, made-to-order sandwiches, recent salads, and even scorching meals bars are not afterthoughts—they’re a part of a rising meal technique. Contemplate Buc-ee’s, the Texas-based gasoline station chain whose meals choice is so widespread that it evokes resale markets and fan pages. Clients spend a exceptional 21 minutes on common in its shops, based on The Hustle, indicating that Buc-ee’s presents an expertise, not only a super-sized drink for the highway.

What’s At Stake for Eating places?

Whereas our Q1 survey discovered some diners had been visiting QSRs extra regularly, almost 40 p.c throughout generations mentioned they had been spending much less at these eating places. This implies that whereas visitors might not have totally dropped off, prospects are reevaluating the worth equation.

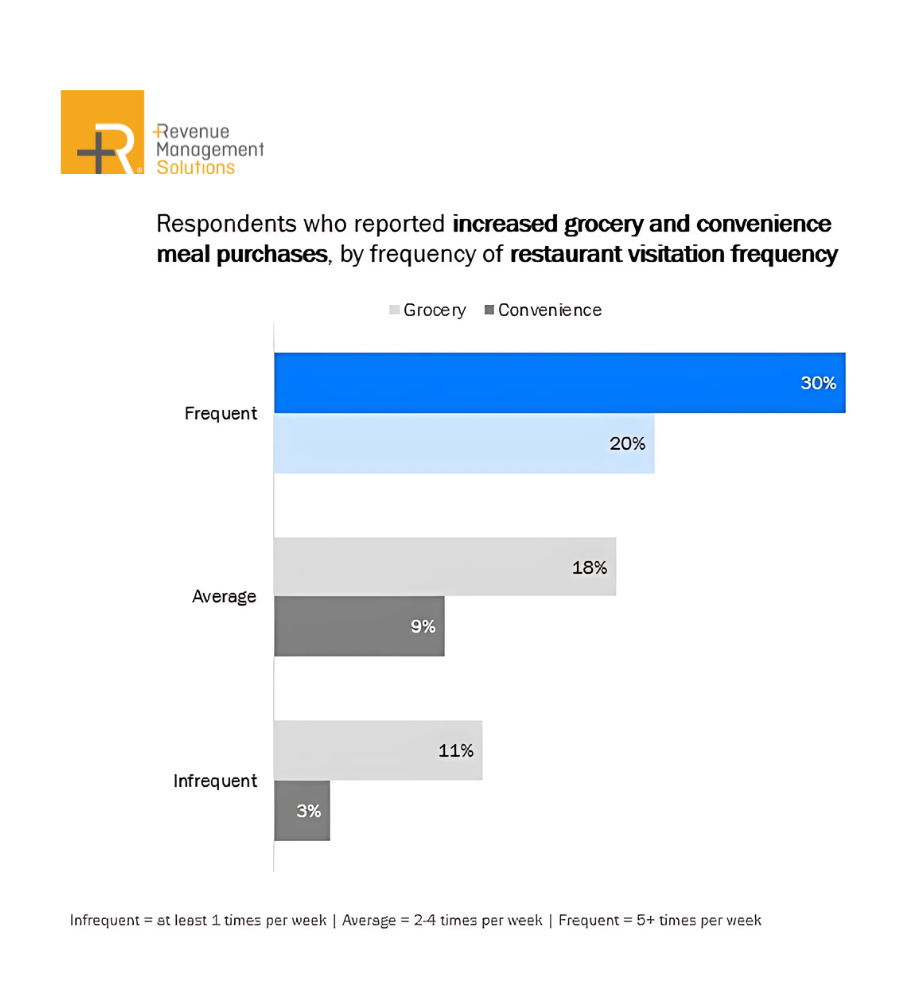

Much more regarding, high-frequency restaurant customers, these consuming out 5 or extra instances per week, had been the most certainly to extend their grocery and comfort retailer meal purchases. Which means eating places are dropping extra than simply the occasional diner; they’re dropping their core prospects.

Including strain, worth perceptions stay excessive. Nearly 4 out of 5 RMS respondents really feel restaurant and grocery costs have elevated in comparison with the earlier month. Knowledge from the U.S. Bureau of Labor Statistics exhibits restaurant worth will increase proceed to outpace grocery inflation. In a time of financial pressure, the notion of a greater deal, even by a greenback or two, can simply tip the scales.

Classes from the Aisles

Retailers aren’t simply providing comfort; they’re enhancing the expertise. Sheetz plans to open 60+ made-to-order meals shops in Michigan, whereas 7-Eleven is increasing food-focused codecs throughout North America. These manufacturers are flipping a web page from the restaurant playbook with quicker service, much less overhead, and, typically, decrease costs.

To compete, eating places should rethink their method. This contains:

- Reexamine the Worth Equation:

With 40 p.c of all respondents saying they’re spending much less on eating out, eating places should clearly show the worth behind each menu merchandise. That does not at all times imply decrease costs. Portion measurement, high quality components, bundled offers, or loyalty rewards can reinforce perceived worth. - Streamline the Buyer Journey:

Operators can study loads from the comfort of comfort shops. Whereas full desk service stays a differentiator, eating places must also consider friction factors in ordering, pickup, or drive-thru experiences. RMS’ Value Studio and different AI-powered instruments will help determine the place efficiencies may improve margins and visitor satisfaction. - Pay Consideration to Meal Varieties and Codecs:

RMS discovered that the highest grocery meal purchases are frozen meals, drinks and ready-to-eat gadgets. Eating places can compete by providing versatile, moveable or refrigerated take-home choices that meet the identical “grab-and-go” want whereas delivering restaurant-quality style. - Know Your Most At-Danger Friends:

RMS knowledge exhibits that frequent restaurant customers are the most certainly to extend their grocery and comfort retailer visits, and Gen Z and millennials are particularly drawn to those shops. That is a purple flag for operators. Your most loyal and certain prospects could also be quietly drifting towards rivals. Focused promotions, customized presents, or loyalty perks might assist pull these buyer sorts again.

What’s Subsequent?

As retail choices enter the race, operators ought to bear in mind this is not only a worth warfare. It is a name to redefine worth. For eating places, meaning asking: What can we provide that retail cannot? And the way can we talk that clearly to a cost-conscious, convenience-driven buyer?