Weekly highlights

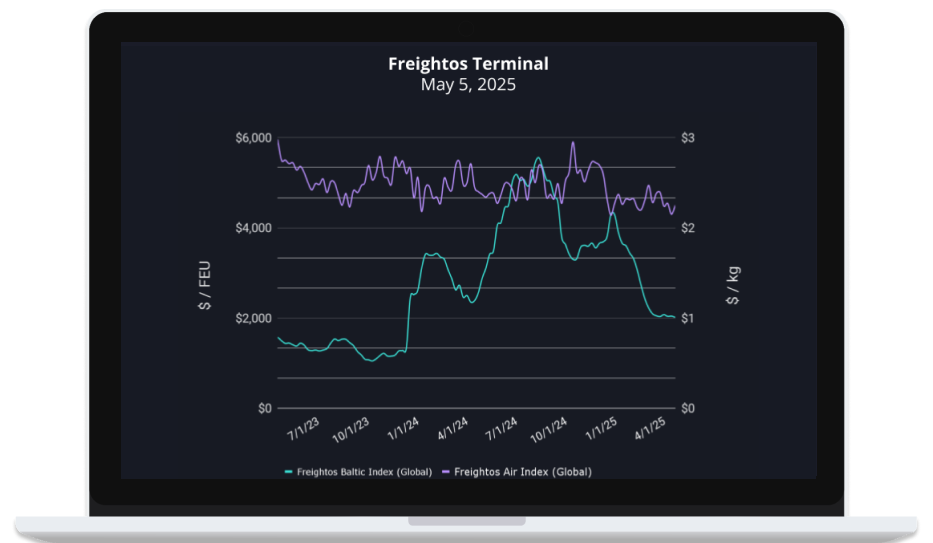

- Asia-US West Coast costs (FBX01 Weekly) stayed stage at $2,321/FEU.

- Asia-US East Coast costs (FBX03 Weekly) stayed stage at $3,386/FEU.

- Asia-N. Europe costs (FBX11 Weekly) fell 3% to $2,261/FEU.

- Asia-Mediterranean costs (FBX13 Weekly) fell 2% to $3,027/FEU.

- China – N. America weekly costs fell 5% to $5.28/kg.

- China – N. Europe weekly costs fell 6% to $3.49/kg.

- N. Europe – N. America weekly costs fell 5% to $1.91/kg.

Evaluation

US tariffs on China – launched after which rapidly raised to 145% in early April – are already inflicting ache to the US logistics market and to shippers whose first items topic to those tariffs are beginning to arrive at US ports.

The tariff hike has pushed a pointy drop in China – US container flows with manufacturing in China additionally being negatively impacted. And even with a 90-day tariff pause for a lot of different US buying and selling companions and the US’s latest easing of phrases for auto tariffs, some nations, like Taiwan and Korea the place automotive items make up a major share of exports to the US, are seeing manufacturing take a success as nicely.

Many US importers have paused orders out of China, however shippers (in addition to producers) can maintain out solely so lengthy earlier than customers will begin to see empty cabinets or increased costs.

There are studies that some main US retailers have already restarted ordering from China, both out of necessity or anticipation that tariff ranges can be decrease by the point of arrival because the US and China get nearer to direct negotiations. In any case, the discount in US sourcing from China for the previous couple of weeks will begin to be felt quickly in fewer Could container ship arrivals and decrease import volumes.

The pause can also be elevating considerations over what’s going to occur if US tariffs on China are decreased and volumes rapidly rebound. The longer the pause the extra disruptive the potential surge – within the type of elevated container charges and doable congestion – is perhaps.

Within the meantime, the White Home continues to specific curiosity in negotiations that would scale back tariffs on an extended checklist of buying and selling companions earlier than the 90-day pause on reciprocal tariffs ends in July, with the European Union being requested, for instance, to purchase extra US items as a part of their deal.

Regardless of dropping volumes out of China and a few improve in demand out of different nations like Vietnam, transpacific container charges have been stage this week as carriers have efficiently decreased capability to present quantity ranges via a vital variety of blanked sailings and repair changes.

Regardless of persistent congestion at a number of main container hubs in Europe which usually places upward stress on container charges, Asia – Europe spot costs dipped barely final week, presumably as a result of a rise in capability as carriers shift transpacific vessels to those lanes.

Carriers are shifting now-excess transpacific capability to different trades just like the transatlantic and Center East too, which might additional complicate a easy restart of China – US volumes as vessels can be out of place.

With the present capability administration measures in place, regardless of the latest commerce warfare induced volatility, carriers have succeeded in holding charges about 50% increased than in 2019 on the main lanes with Purple Sea diversions additionally serving to to soak up capability. Besides, charges on these trades are round 30% decrease than final yr as a result of fleet progress and elevated competitors between the just lately launched provider alliances.

Although a speedy return of container visitors to the Purple Sea within the close to future might be nonetheless unlikely, President Trump’s announcement yesterday that the US reached a ceasefire cope with the Houthis is essentially the most vital change to the established order because the group pledged to solely goal Israeli ships through the Israel-Hamas ceasefire early this yr. Houthi statements point out they are going to stop concentrating on US vessels as lengthy the US holds off assaults on Houthi positions in Yemen, however they promise to proceed assaults on Israel and it’s unclear what all this implies for vessels from different nations.

Container carriers gained’t return to the Suez till there’s readability and so they really feel assured of secure passage, however after they do resume visitors on this lane the shorter voyage will – after an adjustment interval – launch a major quantity of capability again into the market, rising the prospect that carriers will face oversupply and powerful downward stress on charges.

Following the US’s suspension of de minimis eligibility for Chinese language items final week, Temu introduced it’s going to now not ship items immediately from China to US clients. This transfer implies a major shift away from air cargo for China-US e-commerce and to ocean freight and home achievement in an effort to keep away from tariffs so long as doable, scale back prices from air cargo, or shift the tariff burden to home sellers.

The B2C e-commerce shift away from air cargo has resulted in a pointy drop in China – US air volumes – as a lot as two million kilo per day – mirrored in a 30% capability lower because the suspension. However as e-commerce shipments from these platforms traveled principally in chartered freighters, as constitution and different capability is being faraway from this lane, and as spot demand from different sectors – like many electronics exempt from tariffs for now – should be comparatively sturdy, spot charges have but to break down.

Freightos Air Index China – US charges eased solely 5% final week to a nonetheless nicely above regular $5.28/kg. And as Temu and Shein shift a few of their focus to different markets, carriers have began shifting capability to different lanes as nicely. This capability shift might partly clarify China – Europe charges falling to lower than $3.50/kg final week, their lowest stage since early March. Transatlantic charges of $1.90/kg are greater than 20% decrease than in late March, presumably from capability additions as nicely.

Sebastien Podgorski, VP of Airline Options at WebCargo by Freightos, explains that because the lion’s share of the e-commerce impact was felt by charterers, many carriers are literally reporting a latest bump in volumes general, pushed partly by an ocean to air shift from shippers seeking to beat tariff roll outs.

Be a part of 50k+ subscribers who get our free freight weekly replace

“*” signifies required fields