What occurs whenever you discover a profitable, de-risked cope with an skilled operator…and your normal deal construction is totally unusable?

We’ve been going upmarket. Nothing beneath $50K buy value, $150K+ most popular. Extra skilled operators. Much less quantity, better absolute returns.

For higher-value offers (tough guideline: something above ~$200K to $250K buy value)…they virtually all the time include better complexity from due diligence, value-add, regulatory, and/or structuring views.

(Not all the time, as it’s possible you’ll often discover a big acreage tract or a luxurious infill lot above that value that’s comparatively easy. On the flip aspect, messy title offers could require huge effort to amass, with a decrease buy value.)

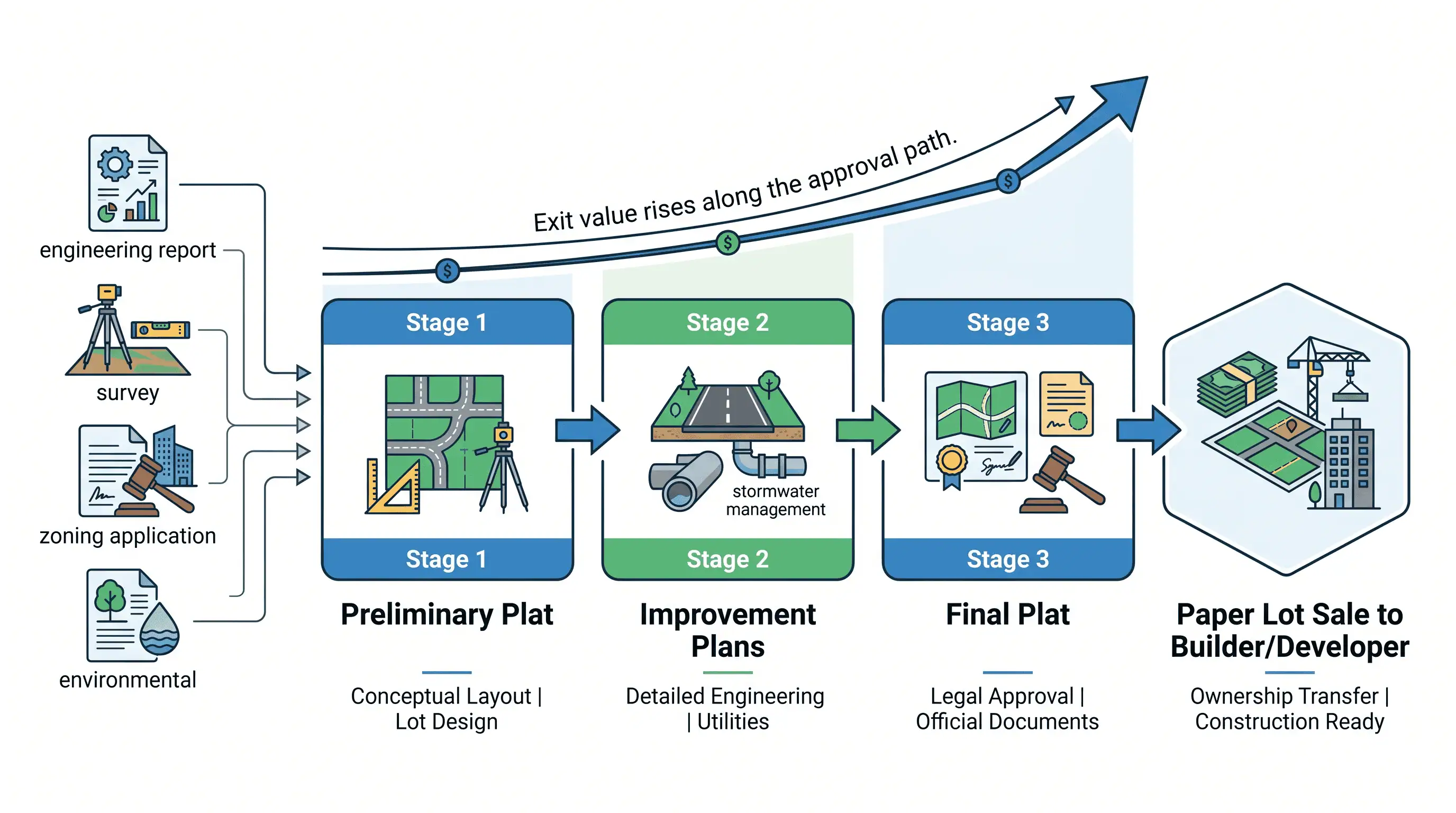

Fast Breakdown on Entitlement Offers

A deal sort we’ve been spending lots of time on just lately is entitlement offers…particularly, funding the gentle prices (e.g., engineering studies, planning and zoning purposes, surveys, environmental consulting, and many others.) to get main subdivide tasks prepared for a paper lot sale to a developer/builder at numerous levels (e.g., preliminary plat, enchancment plans, remaining plat).

Typically, the exit value will probably be greater the additional down the approval pathway, and infrequently, exits can happen earlier than any approval is granted.

Mushy prices (for the paper lot stage) would possibly vary anyplace from ~$100K to $500K on common (typically much less, typically extra, relying on the challenge). The potential upside? Low seven figures on a lovely asset in a robust location.

The vital threat right here…you usually don’t personal the underlying asset. You might have a purchase order settlement from the preliminary vendor, you’re paying for the entitlement work, and also you’re promoting paper tons to the tip purchaser.

If the client pool dries up, improvement points come up or prices balloon, the vendor bails, and/or the native planning authority nixes your plan…your invested capital goes to zero, with no recourse.

The higher model of this play (and a requirement for us to contemplate funding) is to have the tip purchaser already lined up (with a signed LOI, at minimal) earlier than you begin incurring gentle prices. Reduces timeline and market threat, and provides you a a lot clearer image of precise returns.

(And the best possible model is having the tip purchaser fund ALL the gentle prices, along with the EMD and land acquisition prices, whilst you nonetheless take a reduce of the earnings for facilitating the deal. That takes a number of years of relationship constructing, and I do know of just one group that has pulled off this mannequin. The overwhelming majority of the time, you’re on the hook for no less than among the gentle value capital.)

The IRA Drawback

We’ve been deep in assessment of among the finest entitlement offers we’ve seen sourced by the aforementioned skilled operator at the beginning of this text, nevertheless…

One downside. An enormous one.

The operator’s investing entity (which already contributed capital and owned the underlying LLCs tied to contracts particular to every deal beneath assessment) was a self-directed IRA (Particular person Retirement Account with self-directed funding authority), which comes with an entire checklist of prohibitions across the proprietor’s means to personally assure investments or have any of their different property cross-collateralize the IRA’s offers.

Our most popular construction? An working mortgage with a restricted recourse (e.g., unhealthy actor clauses) private assure.

Fully unusable on this state of affairs.

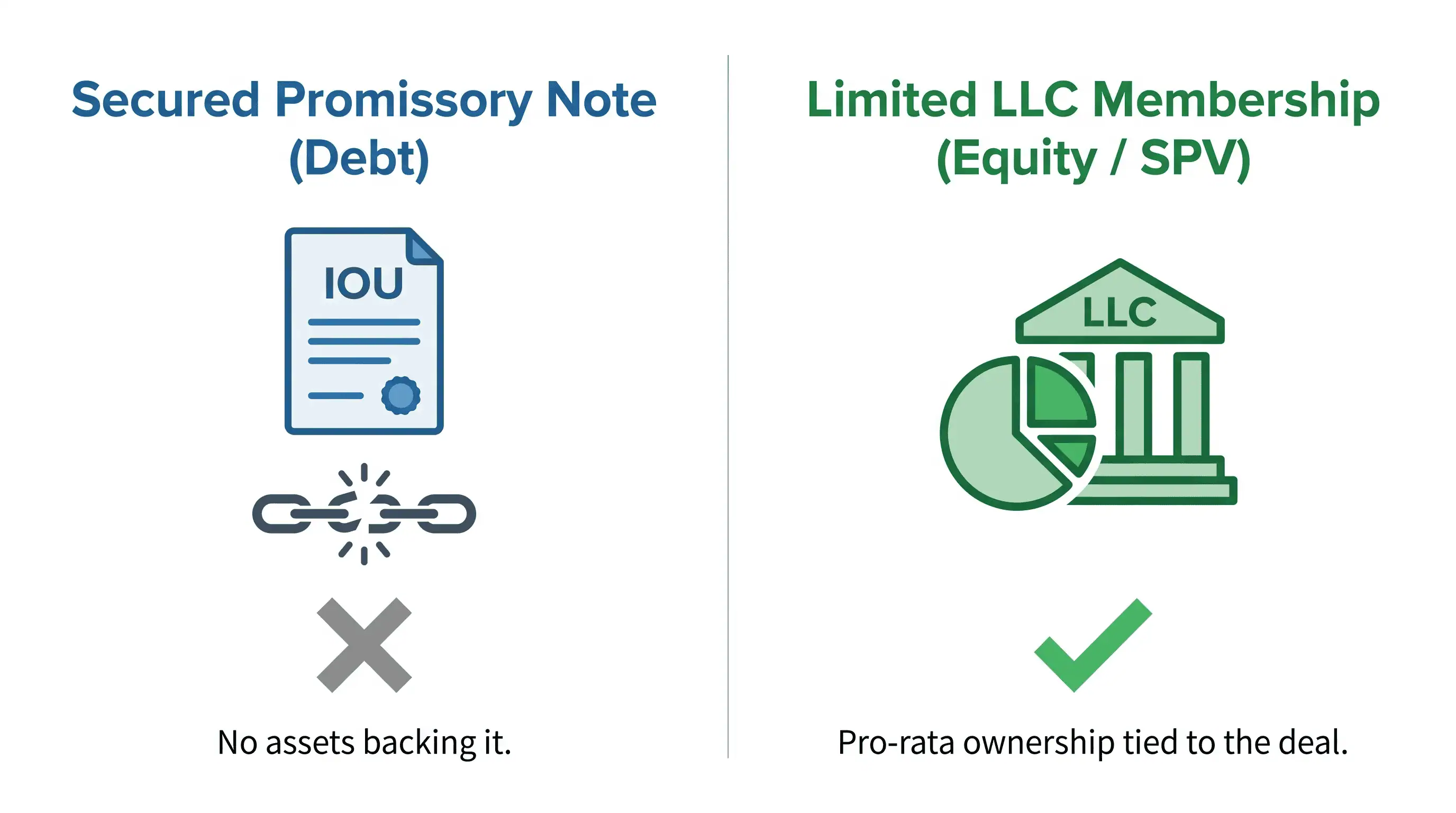

When Debt Turns into Nugatory

So we checked out a unique debt construction, within the type of a secured promissory observe.

With out the flexibility to cross-collateralize something with the operator personally, the debt was successfully nugatory. If the deal went south beneath a limited-recourse construction, there can be no underlying property for us to pursue. The paper says we’re owed cash, however there’s nothing backing it up.

And keep in mind, even with respected finish patrons lined up and a positive approval pathway, these are inherently higher-risk offers with vital complexity… even for restricted capital quantities (in these instances, we have been taking a look at ~$50K–$175K checks).

Rule #1 in investing (any asset class): Don’t lose cash. Each greenback must be deployed rigorously and thoughtfully.

I’ll be trustworthy…I used to be initially extra comfy with the revised debt strategy, and I used to be excited that we have been ‘virtually dwelling’ on a few robust offers in a troublesome market.

However my enterprise accomplice, who has spent a few years engaged on main, advanced company restructurings, simply stored itemizing the the explanation why the debt path and the return profile have been inappropriate from a risk-management standpoint… and he was proper.

(The lesson right here is perhaps simply as vital because the structural one…you’ve received to have the humility to defer to your accomplice’s experience, or when conflicting knowledge is delivered to your consideration, even when it means scrapping hours of labor and beginning over…or doubtlessly shedding out on a deal.

Generally, inertia is your largest enemy. You don’t wish to have to return and rethink all the pieces, so that you rationalize the trail you’re already on. The comfy route is the lazy one. That’s a lure we people have to stay consistently vigilant for.)

The SPV Pivot

So we thought laborious about what might nonetheless make these offers work. We’ve structured investments earlier than utilizing an LLC framework within the type of an SPV (Particular Function Automobile, which is mainly a standalone authorized entity created particularly for a specific funding or challenge), permitting totally different buyers to return in by way of fairness and have possession throughout the SPV.

May we adapt that right here?

Seems…sure. There are not any prohibitions on a self-directed IRA (that may be a sole member of an LLC) from having different buyers come into the LLC as members, as long as we’re not private relations of the operator behind the IRA. So, as an alternative of debt, we structured it in order that our LLC can be a restricted member of the underlying working LLC.

Though we bear the identical threat of the deal falling aside and our invested capital going to zero, we have now precise pro-rata possession of the LLC, which provides us inherently better authorized safety tied to the deal we’re making an attempt to shut, in comparison with debt backed by no property.

Plus, we utilized our promote construction (a performance-based incentive tier that enhances upside to the first deal operator), much like what we’ve completed on different offers, and is closely weighted towards the monetary good thing about the operator, whereas nonetheless giving us an acceptable return profile for the extent of threat our capital is uncovered to. No private assure wanted. And no UCC-1 submitting wanted (that’s a recorded lien filed towards an entity incurring debt, mainly a public tracker in county data).

Cleaner. Extra protecting. Higher aligned with the precise threat profile.

The Payoff

After a few hours, we frolicked reformatting the construction and massaging the messaging… the operator agreed to the framework.

That’s the half I’m most enthusiastic about. An skilled operator who trusts us sufficient to work by way of a totally restructured deal, and who understands that we’re (essentially) sticklers on documentation and threat administration, all in favor of constructing long-term, sustainable partnerships.

(Actual property is rife with freewheeling dealmakers, backing outcomes with handshakes as an alternative of paperwork, and that can come again to chunk them earlier than later…if it hasn’t already. I’ve realized that the laborious approach, a narrative for one more time.)

The broader takeaway? Larger-level offers require higher-level problem-solving. AI is an enormous lever (I exploit it extensively to suppose by way of construction and authorized settlement changes), but it surely gained’t rescue you when you don’t perceive what the tip aim needs to be. The context issues greater than something…and when you don’t even know what query(s) to ask, you’re going to get boilerplate nonsense again.

The willingness to do the laborious work…the artistic structuring, the uncomfortable back-and-forth between companions and operators, the scrapping of hours of prior effort when the scenario requires it, the potential to place apart ego (most likely the HARDEST half for many entrepreneurs)…that’s the place you’ll earn the returns most people won’t ever hassle to combat for.

Want a capital accomplice who does the additional work on deal structuring and documentation, for long-term, mutual success? We’ve funded over $6.5M in land offers with industry-leading 41% working margins, and we shut 100% of offers we decide to. $50K+ test sizes. Nationwide underwriting expertise on each transaction.

When you’re an skilled operator with a gradual deal movement and also you desire a accomplice who gained’t reduce corners… let’s speak.

Get Your Property Analyzed Immediately

Initially revealed at SeriousLand.capital on February 16, 2026.